Start with Insights

Before designing anything, ten sprint questions framed the problem space, covering the user, the product, the experience over time and the principles that will govern every decision.

How might we help an emerging affluent customer build financial literacy and develop sustainable habits through guidance that feels personal, not prescriptive?

Sprint Questions

What do we need to understand before we design? Ten questions frame the problem space.

Who are we designing for?

Five personas across the customer spectrum. Amara is the primary ICP — the largest and most designable audience.

Where does financial behaviour actually come from?

Five bodies of evidence on why people manage money the way they do — and what actually changes behaviour. The research foundation for the financial-habit library.

Financial habit sources

5 sources. 2 layers. Structural habits set the architecture of good finances; behavioural habits make them stick, each grounded in behavioural evidence, with product context.

| Layer | Area | The habit | Behaviours & habits | Evidence | Why it works |

|---|---|---|---|---|---|

| Core | Foundation | Spend less than you earn | Track the gap between income and outgoings. Make the surplus visible without shame. app: spending overview | Consistency over intensity (Housel) | Behaviour beats income — a modest, consistent surplus compounds; occasional heroics don't. |

| Core | Stability | Pay your bills on time | Automate essentials. Buffer before due dates. app: reminders, auto-pay | Defaults (Thaler) | Removing friction changes behaviour more than willpower ever does. |

| Core | Safety | Have an emergency fund | Start small, automate it, ring-fence it. 1 → 3 → 6 months. app: goal pot | Loss aversion (Kahneman) | Framed as protection from loss, not sacrifice — which is what actually motivates saving. |

| Core | Growth | Start investing | Begin once stable. Small, regular, automated. Time in the market over timing it. app: goal setting | Present bias (behavioural econ) | Making the future feel present overcomes the pull of now. |

| Core | Protection | Protect yourself | Cover catastrophic risks first. Right-size, don't over-buy. Review at life events. app: coverage check | Honest over optimistic (trust) | Name real risk without fear-selling. Proportional confidence, not scare tactics. |

| Core | Optimisation | Make your money work | Tax efficiency, fees, rebalancing, compounding. app: portfolio view | Depth for the engaged (Clear) | Layer sophistication for those who want it, without overwhelming the majority. |

| Behavioural | Automation | Automate the decision | Pay yourself first. Set-and-forget transfers. Remove willpower from the loop. app: automated rules | Defaults & friction (Thaler / Clear) | The highest-leverage habit — good behaviour by default doesn't depend on motivation. |

| Behavioural | Awareness | Check in without avoiding | Build a regular, low-anxiety habit of looking at your money — even when uncomfortable. app: gentle check-in | Shame & avoidance research | Avoidance is the core failure mode. People stop looking when they most need to. |

| Behavioural | Restraint | Pause before spending | Introduce friction before non-essential purchases — the 24-hour rule. app: spend prompt | Present bias (Kahneman) | A small delay counters the present-bias pull that drives impulse spending. |

| Behavioural | Purpose | Set a meaningful goal | Define what money is for — not a number, a purpose. Measure progress against it. app: goal setting | Define your "enough" (Housel) | Purpose sustains behaviour where willpower fails. |

| Behavioural | Resilience | Recover, don't abandon | Treat an overspend or missed month as data, not failure. Re-engage without shame. app: setback reframe | Shame & avoidance research | The setback moment is where products lose people. A shame-free reframe is the biggest differentiator. |

How trust is built

How does the experience build trust over time — and what prevents false confidence or misinterpretation when the subject is someone's money?

From problem to opportunity

The experience mapped across time, key moments in the 30-day arc and a clear happy path.

30-day journey map

What a member feels, needs and does at each critical moment.

11 habits across 2 layers

Grounded in behavioural finance and habit science. Structural habits set the architecture; behavioural habits make them stick. Six form the day-one onboarding set, the habits US Retail Bank should offer on day one.

Tokens & craft

A minimal token set built before any HiFi screen, colour, typography, spacing, radius and components, all calibrated to the US Retail Bank brand.

Extend the Design System with AI Capabilities

The design system doesn't just govern screens, it governs how AI generates content. By encoding the brand, principles and audience into a reusable brief, every AI-produced asset, copy and photography, comes out on-brand, on-tone and honest by default. The system becomes the guardrail that lets AI scale content production without drifting.

Photography

The photography answers one question: does this look like a real person's financial life, or a stock-photo fantasy of wealth? The direction is grounded, diverse and quietly aspirational, never the yacht-and-champagne cliché of finance marketing.

Tone of Voice

The system plugs four inputs into every AI content brief: the design system (visual rules), brand guidelines (voice and identity), the three principles (clarity, consistency, honesty) and the ICP (Emerging Affluent). From that brief, AI generates both copy and photography direction, consistent, on-brand and honest by construction.

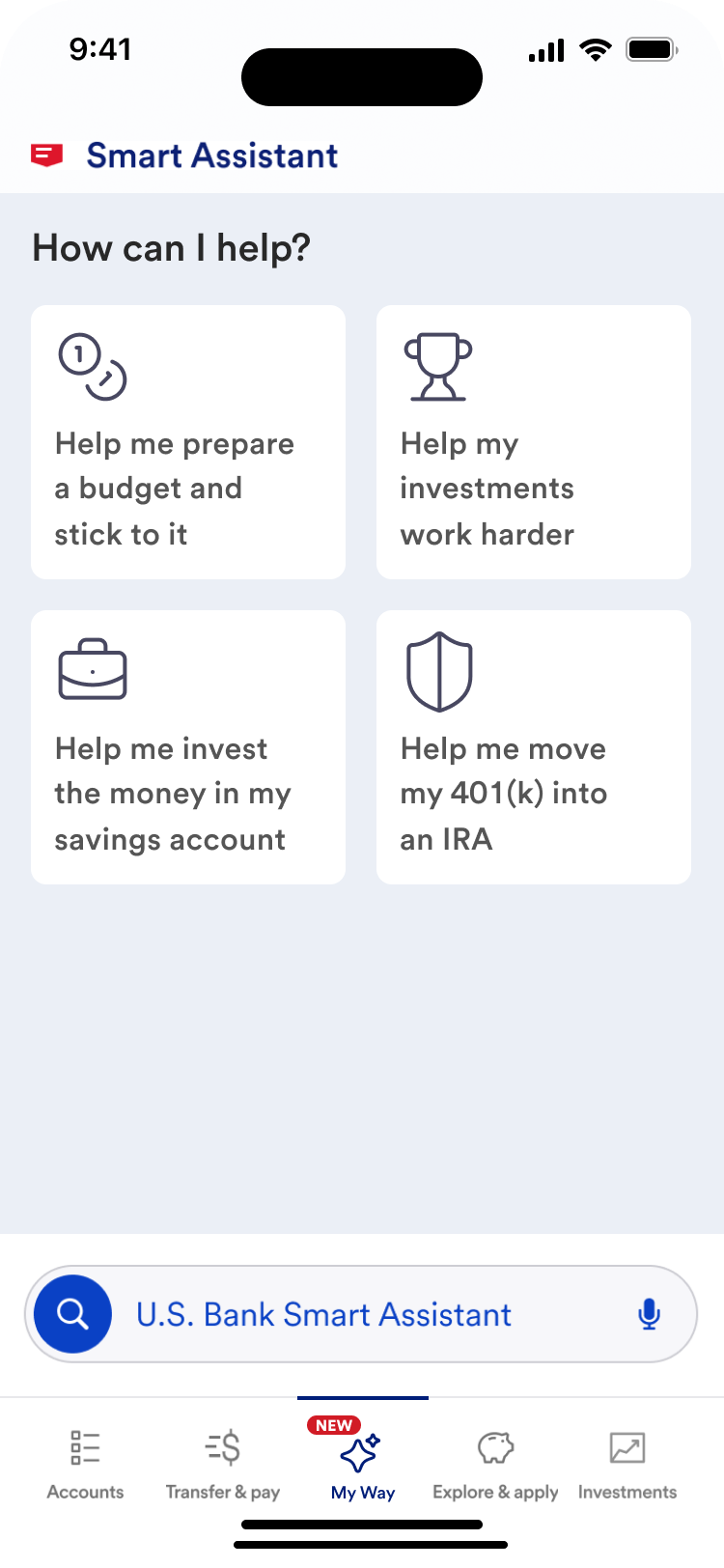

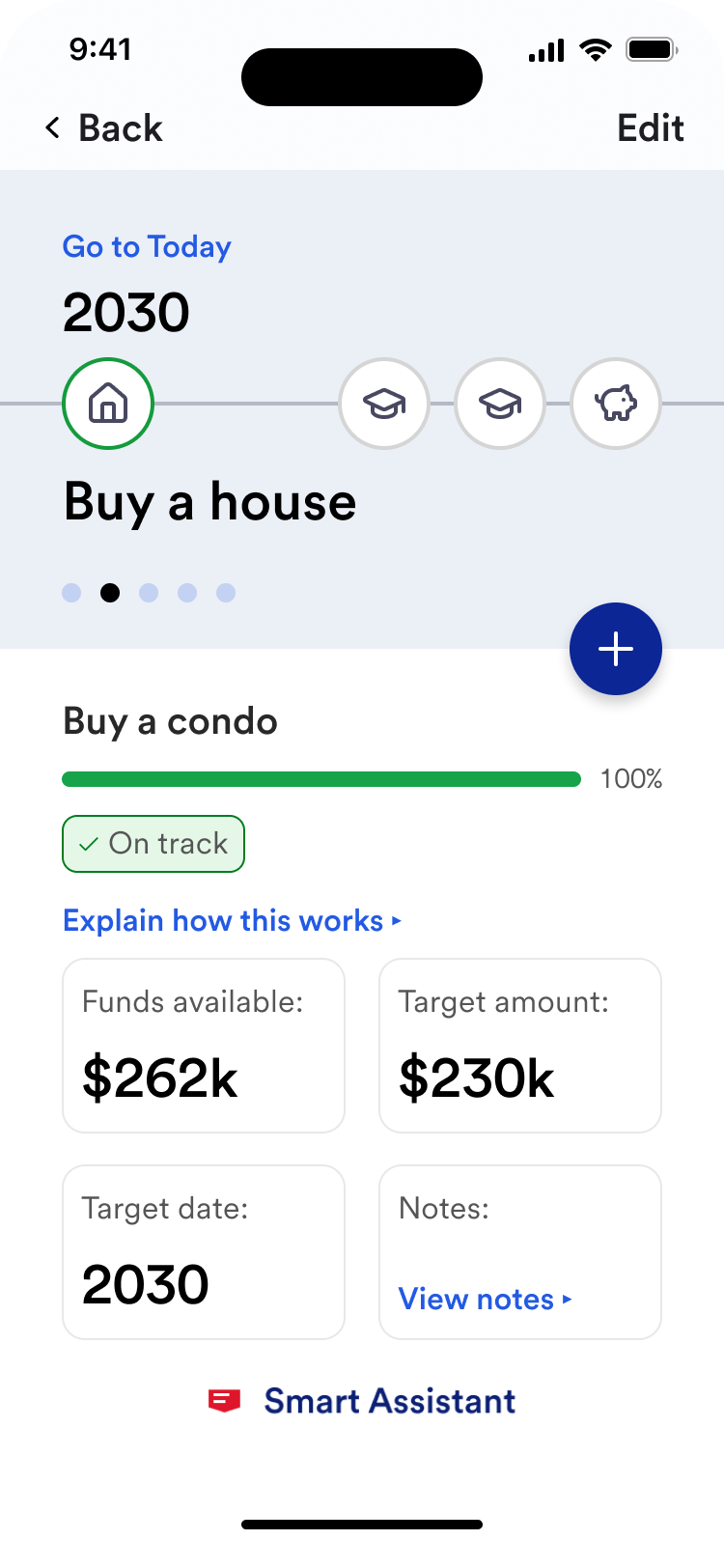

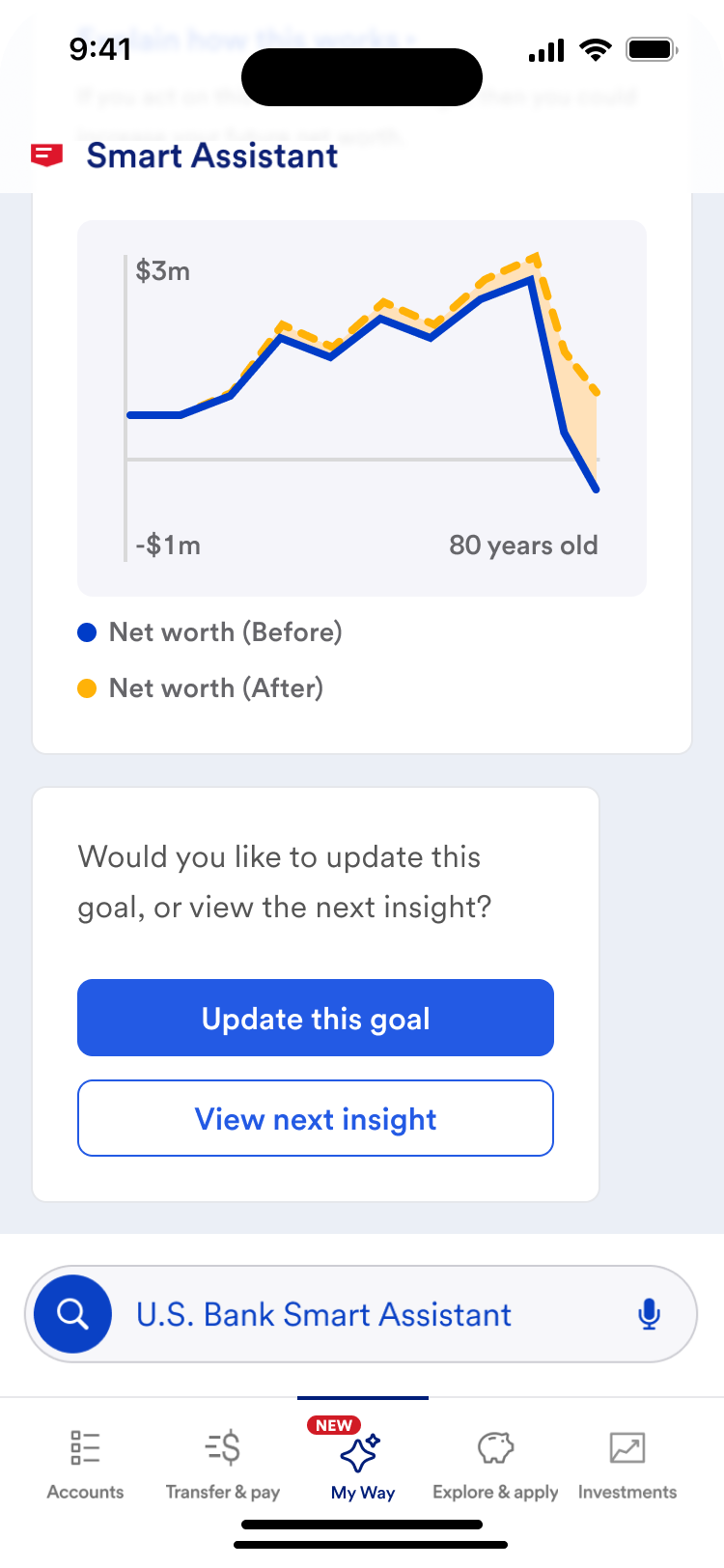

High-fidelity screens

AI woven through the experience, not bolted on. Each screen applies the same discipline: one clear action, evidence-based framing, and language that guides rather than advises. Together they trace the arc from an open question, to a concrete goal, to a personalised insight, to an honest next step, showing how AI can feel like a trusted guide rather than a dashboard to decode.

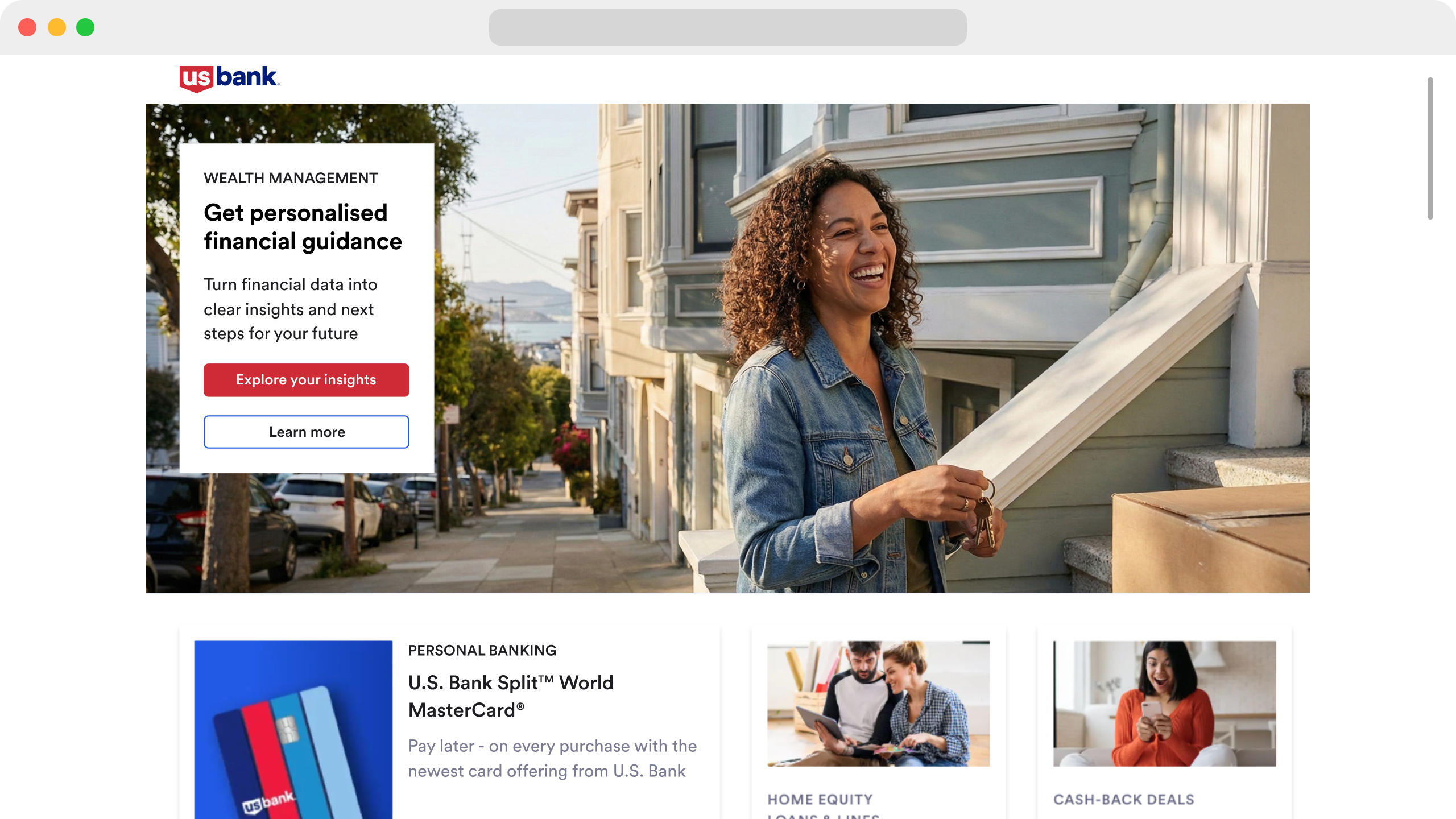

Web experience

The web channel — the same guidance discipline at desktop scale.

Native app

The native app experience — one clear action per screen, honest framing throughout.

Evaluation & Validation with User Testing

Concept validation was the whole point of Discovery: to produce evidence for build, not just designs. Two rounds of targeted testing with the primary segment pressure-tested whether the experience was usable, whether customers understood it and whether it earned their trust. The findings de-risked the build decision with real signal, not assumption.

Research Questions

Two rounds of targeted testing, structured around three question sets.

Next Steps

Three areas for v2 and open questions that discovery didn't answer, but a live product must.